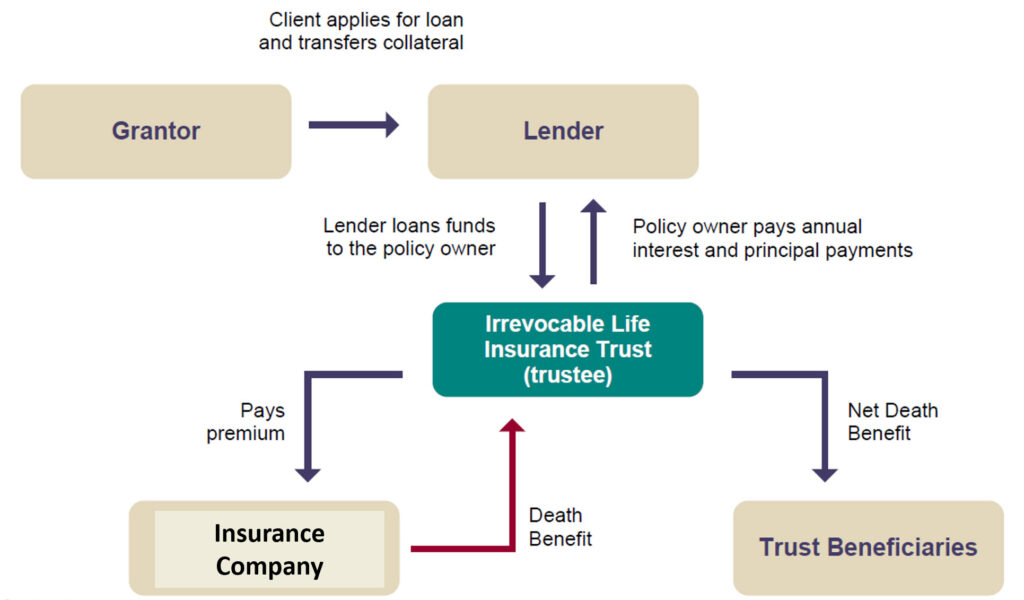

The beauty of Premium Financing is that you can put the bank’s money to work to build tax-free wealth and purchase large amounts of death benefit protection. The cash value grows with no risk of ever losing any money to the market fluctuations.

The catch is that you need to have income and net worth that are high enough to justify the amount of insurance and to afford the interest payments or a portion of it on the loan. If you are borrowing a million dollars at 5% interest, for example, your annual interest expense could be $50,000.

Leverage also increases risk.

Historically, Premium Finance programs have only been made available to people with a five to ten million dollar net worth or more. However, in recent years, programs have been made available for a class of individuals known as “emerging affluent”.

Another con is that the loans must be 100% secured. This means that if $1 of Premium turns into $0.85 of cash value, then the policy owner must have to have other assets to make up the other 15%. This can be accomplished with a letter of credit or an assignment of collateral. This highlights the need for a properly designed and maximum overfunded life insurance policy.

A very big “pro” that is often overlooked is the Disablity Protection like Critical, Chronic, Terminal Illness that the policy provides in the event that the client faces health issues. In this case, instead of tapping into their assets, they can now use the “Death Benefit” within the policy to take care of financial needs.

To overcome the potential “cons”, the policies we design use fairly conservative numbers.